Putting Money in a 529

Who can open or contribute to a 529 Plan?

- Parents

- Grandparents, relatives and friends

- Anyone who wants to support someone’s future education

Family members can open 529 accounts for their relatives. With a few basic facts about the beneficiary, they can get started.

The Education Plan® is flexible too. If one child in a family doesn’t end up needing 529 savings, the money can typically be transferred to another eligible family member without tax consequences.

Before you open an account, decide how you want to contribute. You have a lot of options:

- Send a check – just write a check and mail it with a contribution coupon and we’ll deposit the funds into your account. You can send checks as often as you like.

- One-time electronic funds transfer – you can make a transfer from your bank account.

- Automatic Investment Plan (AIP) – schedule recurring contributions from your bank account. It’s the easiest way to save. Set-up is simple.3

- Payroll contribution – if your employer offers it, you can make a contribution to your 529 Plan directly from the pay you receive from your employment.

- Rollover/transfer from another 529 Plan or Coverdell Education Savings Account/Qualified U.S. Savings Bond – transfer funds from other eligible accounts or investments. We’re happy to help.

As your student grows, so could your 529 account

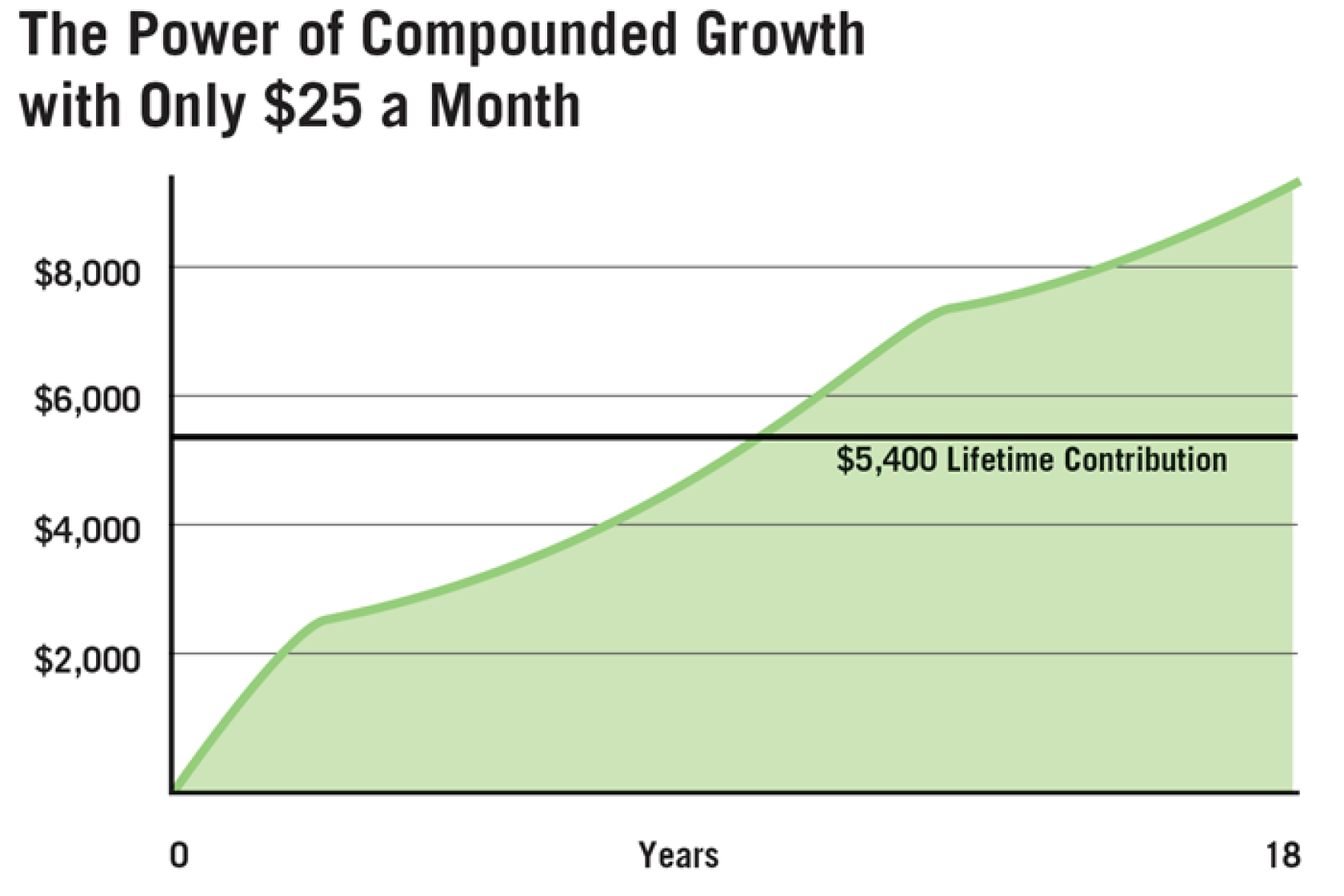

Money in a 529 Plan has tax advantages, is professionally managed, and may benefit from the power of compounded growth. Compounding means that any income earned on your investments in the account has the potential to generate additional income in the next year and each year thereafter. Earnings are automatically reinvested and help the account grow faster.

Total: $8,730

This hypothetical example assumes a 5% annual rate of return on a $25 monthly contribution into a 529 college savings account over 18 years (total lifetime contribution of $5,400). When compounded every year at the same rate of return, the account could grow by 64% and be worth $8,730. The extra $3,330 is the benefit of compounded growth. This chart is for illustrative purposes only and does not represent the performance of any specific account or investment and does not reflect plan costs or sales charges that may apply. If such costs or sales charges had been taken into account, returns would have been lower.

Systematic investing does not assure a profit or protect against loss in declining markets. Before investing, investors should evaluate their long-term financial ability to participate in such a plan.

Frequently Asked Questions

A 529 plan is a tax-advantaged investment account that is designed to grow savings for future education expenses for a specified beneficiary. 529 plans offer unique benefits and features that make them an appealing strategy for education related saving.

A 529 plan can be used for “qualified educational expenses.” For federal tax purposes, qualified educational expenses include:

- Tuition and fees at accredited higher education institutions

- Books

- Supplies and equipment

- Room and board for beneficiaries attending on at least a half-time basis.

- Computer technology, equipment, and internet access

- Up to $10,000 a year for K-12 tuition and expenses (Limit increase to $20,000 in 2026)

- Expenses for educational special needs services

- Transfers to an ABLE account for the beneficiary (transfer subject to annual limit)

- Apprenticeship expenses

- Up to $10,000 for student loan repayment

- Credentialing expenses and certification programs

- Roth IRA rollover for the beneficiary

If you're not sure if an expense is considered "qualified," we recommend consulting with a tax professional or advisor. Unqualified expenses will be treated like ordinary income: state and federal taxes will apply, with a 10% federal penalty for withdrawals from your 529 plan used to pay for them.

New Mexico residents can deduct contributions to The Education Plan from their state taxable income each year. This includes contributions made to an account that you are not the account owner of.

You cannot deduct contributions from federal income taxes.

Any person at least 18 years old with a valid Social Security Number (SSN) or Tax Identification Number (TIN) can open a 529 account. The account holder chooses the investment options, designates a beneficiary, and requests the distribution of funds.

The cost of college continues to rise, including tuition, housing, food and supplies, so it’s important to begin saving as soon as possible. You can learn more about how much a typical college education costs on our Cost of College page. It’s never too early or too late to start.

The Education Plan offers a variety of investment options to fit you and your family’s needs, risk tolerance and goals. You can see all of the available investment portfolios on the investments page.

Yes, you can use up to $20,000* a year to cover tuition and expenses for K-12 education.

Qualified K-12 expenses include:

- Tuition (public, private, and religious)

- Curriculum materials, books (including digital/online) and instructional materials

- Tutoring and instructional classes**

- Fees for a nationally standardized norm-referenced achievement test, an advanced placement examination, or any examinations related to college or university admission

- Dual enrollment program fees

Educational therapies for students with disabilities provided by a licensed or accredited practitioner or provider, including occupational, behavioral, physical, and speech-language therapies

*Starting in tax year 2026. The annual limit is $10,000 in tax year 2025 and permitted for tuition only.

**Tuition for tutoring or educational classes outside of the home, including at a tutoring facility, but only if the tutor or instructor is not related to the student and—

(i) is licensed as a teacher in any State,

(ii) has taught at an eligible educational institution,

or (iii) is a subject matter expert in the relevant subject.

You can open an account with The Education Plan online or by mailing in the enrollment form. In order to open an account, you will need the following information:

- Your social security number or TIN

- Your address

- Your bank account information (in order to fund the account)

- The beneficiary’s social security number or TIN

- The beneficiary’s birthday

-The beneficiary’s address