What is a Year of Enrollment Portfolio?

If you’re like many parents and caregivers, you’re busy. The thought of managing an investment portfolio for your loved one’s future education may not sound like a super fun thing to add to your to-do list. Don’t worry. We get it.

We know that choosing investment options can be overwhelming, but The Education Plan® can help make it easy. We offer a range of professionally managed investment options to fit your needs and risk tolerance, and you can choose how hands-on or hands-off you want to be with your investments.*

Choosing a 529 Investment Portfolio

Before you invest, you’ll want to consider two main things:

-

Your education savings goals. Whichever portfolio you choose, the funds in a 529 account with The Education Plan can be used for a variety of educational needs, including K-12 tuition, college tuition, apprenticeship programs, graduate school, medical and law school, and more. Consider how and when you will use the funds in your account.

-

Your risk tolerance. Many families investing in 529 plans for future education want to strike a balance between playing it safe and aiming for growth. New parents probably have a very different education savings strategy than those whose children are closer to college age. When their children are young, parents may prefer more aggressive investments that offer a higher potential for long-term growth as well as risk. As their children approach college age, these same parents may choose more conservative investments that prioritize preserving their savings. Our Year of Enrollment Portfolios can help you manage your funds with this approach in mind.

*Investment returns will vary depending upon the performance of the investment portfolios you choose. You could lose all or a portion of your money by investing in The Education Plan depending on market conditions. Account owners assume all investment risks as well as responsibility for any federal and state tax consequences. We recommend consulting with a financial, tax or other advisor about your specific situation before investing.

At The Education Plan, there are three basic portfolio options. These include:

Individual Portfolios Generally, this approach is for investors who are comfortable selecting their own investment strategy and prefer more control over their investments. Five individual portfolios are available to create your own personalized investment mix.

These portfolios consist of a single underlying fund comprising a mix of similar investments and risk levels: U.S. equity (stock), Bonds, a Short-term Treasury portfolio, a Responsible Equity Portfolio, and a Capital Preservation Portfolio. Additional information on these funds, portfolio fees, and more is available on The Education Plan's website.

Allocation Portfolios. The Education Plan offers eight allocation-based portfolios consisting of a mix of underlying funds designed to match a desired risk level.

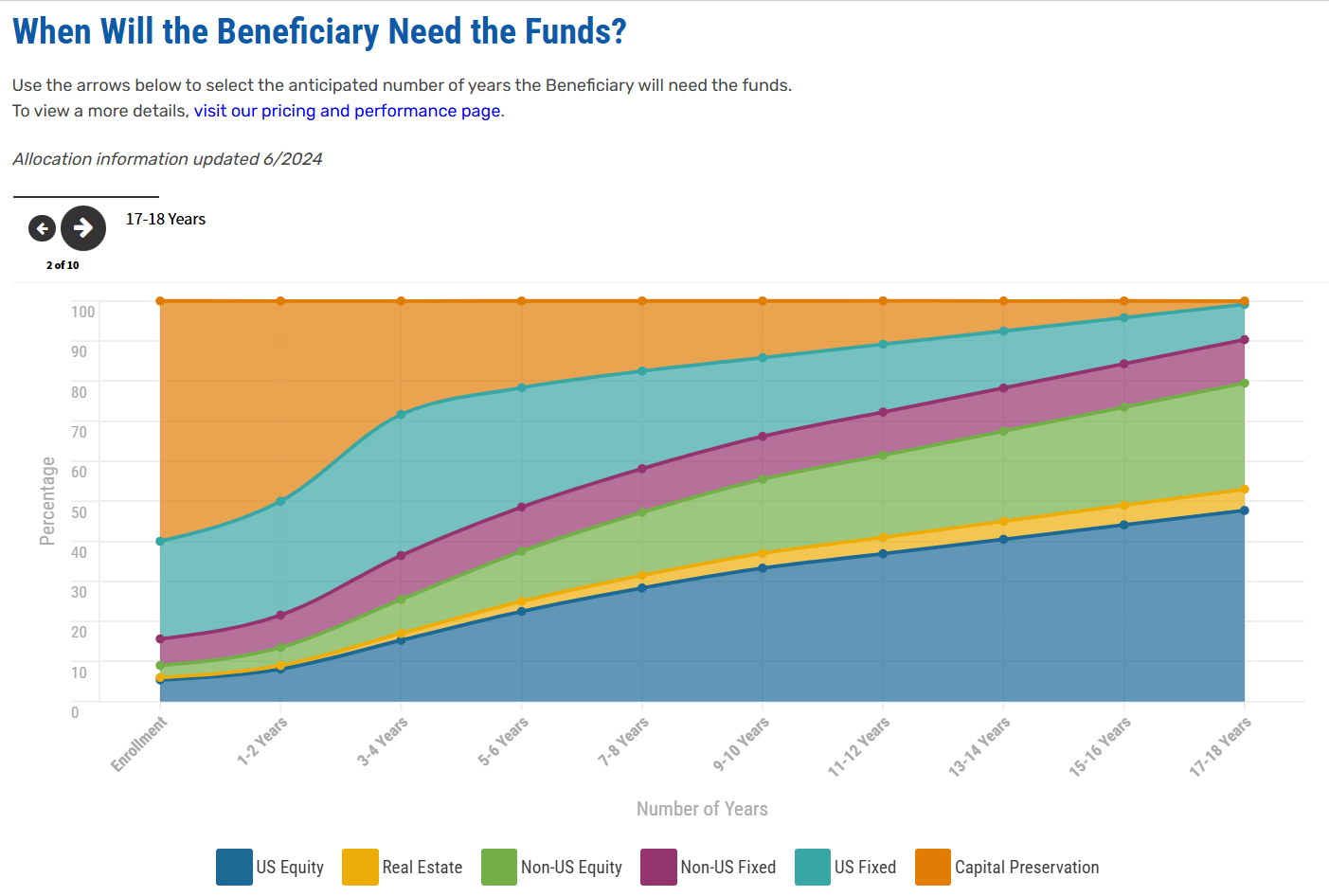

Year of Enrollment Portfolios. This approach is based on the beneficiary’s year of enrollment. It consists of a blend of investments, assuming enrollment at age 18, that automatically changes to match the shortening time horizon and appropriate risk levels.

How Year of Enrollment Portfolios Work.

The Education Plan offers 11 different Year of Enrollment portfolios based on your beneficiary's anticipated enrollment date. The enrollment date is the year you anticipate your loved one will need to start using the savings in the account.

Investment options include funds focusing on a mix of U.S. stocks, fixed income, real estate, and capital preservation. You can see pricing and performance information on all available funds before you make decisions on how to invest.

If you choose the Year of Enrollment portfolio option, simply select the year you believe your beneficiary will need their savings for future education. For example, if you're opening a plan for an infant born in 2024, their anticipated year of enrollment would be 2042, when they turn 18.

Year of Enrollment portfolios are designed to make investing for your loved one’s future education easier. These portfolios will automatically rebalance your investments, opting for more conservative investments as your loved one’s age of enrollment approaches.

You can see the glidepath that is used to adjust the investment mix for a time horizon of 17-18 years. Visit our Investment page to see an interactive glide path that allows you to see how your portfolio's investment mix will change over time.

It’s Never Too Early or Too Late to Start Saving.

The best time to start saving for future education is now. It takes about 15 minutes to start saving with a 529 account with The Education Plan. You'll need the following information to get started:

-

Beneficiary’s Date of Birth

-

Beneficiary's Social Security or Tax Identification Number (TIN)

-

Your Social Security Number

-

Your U.S. Street Address (not P.O. Box)

-

Your Bank Routing Number

Ready to start saving? Sign up for an account today!

Frequently Asked Questions

A 529 plan is a tax-advantaged investment account that is designed to grow savings for future education expenses for a specified beneficiary. 529 plans offer unique benefits and features that make them an appealing strategy for education related saving.

A 529 plan can be used for “qualified educational expenses.” For federal tax purposes, qualified educational expenses include:

- Tuition and fees at accredited higher education institutions

- Books

- Supplies and equipment

- Room and board for beneficiaries attending on at least a half-time basis.

- Computer technology, equipment, and internet access

- Up to $10,000 a year for K-12 tuition and expenses (Limit increase to $20,000 in 2026)

- Expenses for educational special needs services

- Transfers to an ABLE account for the beneficiary (transfer subject to annual limit)

- Apprenticeship expenses

- Up to $10,000 for student loan repayment

- Credentialing expenses and certification programs

- Roth IRA rollover for the beneficiary

If you're not sure if an expense is considered "qualified," we recommend consulting with a tax professional or advisor. Unqualified expenses will be treated like ordinary income: state and federal taxes will apply, with a 10% federal penalty for withdrawals from your 529 plan used to pay for them.

New Mexico residents can deduct contributions to The Education Plan from their state taxable income each year. This includes contributions made to an account that you are not the account owner of.

You cannot deduct contributions from federal income taxes.

Any person at least 18 years old with a valid Social Security Number (SSN) or Tax Identification Number (TIN) can open a 529 account. The account holder chooses the investment options, designates a beneficiary, and requests the distribution of funds.

The cost of college continues to rise, including tuition, housing, food and supplies, so it’s important to begin saving as soon as possible. You can learn more about how much a typical college education costs on our Cost of College page. It’s never too early or too late to start.

The Education Plan offers a variety of investment options to fit you and your family’s needs, risk tolerance and goals. You can see all of the available investment portfolios on the investments page.

Yes, you can use up to $20,000* a year to cover tuition and expenses for K-12 education.

Qualified K-12 expenses include:

- Tuition (public, private, and religious)

- Curriculum materials, books (including digital/online) and instructional materials

- Tutoring and instructional classes**

- Fees for a nationally standardized norm-referenced achievement test, an advanced placement examination, or any examinations related to college or university admission

- Dual enrollment program fees

Educational therapies for students with disabilities provided by a licensed or accredited practitioner or provider, including occupational, behavioral, physical, and speech-language therapies

*Starting in tax year 2026. The annual limit is $10,000 in tax year 2025 and permitted for tuition only.

**Tuition for tutoring or educational classes outside of the home, including at a tutoring facility, but only if the tutor or instructor is not related to the student and—

(i) is licensed as a teacher in any State,

(ii) has taught at an eligible educational institution,

or (iii) is a subject matter expert in the relevant subject.

You can open an account with The Education Plan online or by mailing in the enrollment form. In order to open an account, you will need the following information:

- Your social security number or TIN

- Your address

- Your bank account information (in order to fund the account)

- The beneficiary’s social security number or TIN

- The beneficiary’s birthday

-The beneficiary’s address